For many property owners, roofing projects are treated as standard capital improvements. A contract is signed, a deposit is issued, work begins—and the expectation is simple: the job will be completed as agreed.

In reality, there is a less discussed but very real risk in the roofing industry: contractor failure during or after a project.

Whether due to financial instability, operational issues, or business closure, contractor disappearance is not a rare edge case—it is a scenario every property owner should factor into project planning.

The Hidden Risk Behind Roofing Contracts

Roofing is structurally a high-cash-flow, high-expense industry. Most projects involve:

- upfront material procurement

- mobilization of labor crews

- staged progress payments tied to milestones

This structure creates vulnerability points where projects can be interrupted if a contractor experiences financial or operational breakdown.

When that happens, property owners are often left with:

- partially completed roofs

- unresolved defects

- limited legal or practical recourse

In many cases, restarting the project means paying twice.

Why Standard Warranties Often Fail in Practice

One of the most common misunderstandings in roofing is the belief that a contractor warranty guarantees long-term protection.

In practice, most workmanship warranties depend entirely on the continued existence of the contractor who issued them.

If the company closes or becomes insolvent:

- the workmanship warranty is effectively void

- enforcement becomes nearly impossible

Material warranties may still exist, but they typically cover only product defects—not installation errors or system-level failures.

This creates a structural gap between what property owners expect and what is actually protected.

The Industry Gap: When Protection Depends on One Company

Traditional roofing risk is binary: either the contractor completes the job, or they don’t.

But modern project environments show a different reality:

contractor stability is no longer guaranteed over the lifecycle of a project or warranty period.

This has led to increasing demand for additional protection layers that are independent of the contractor itself.

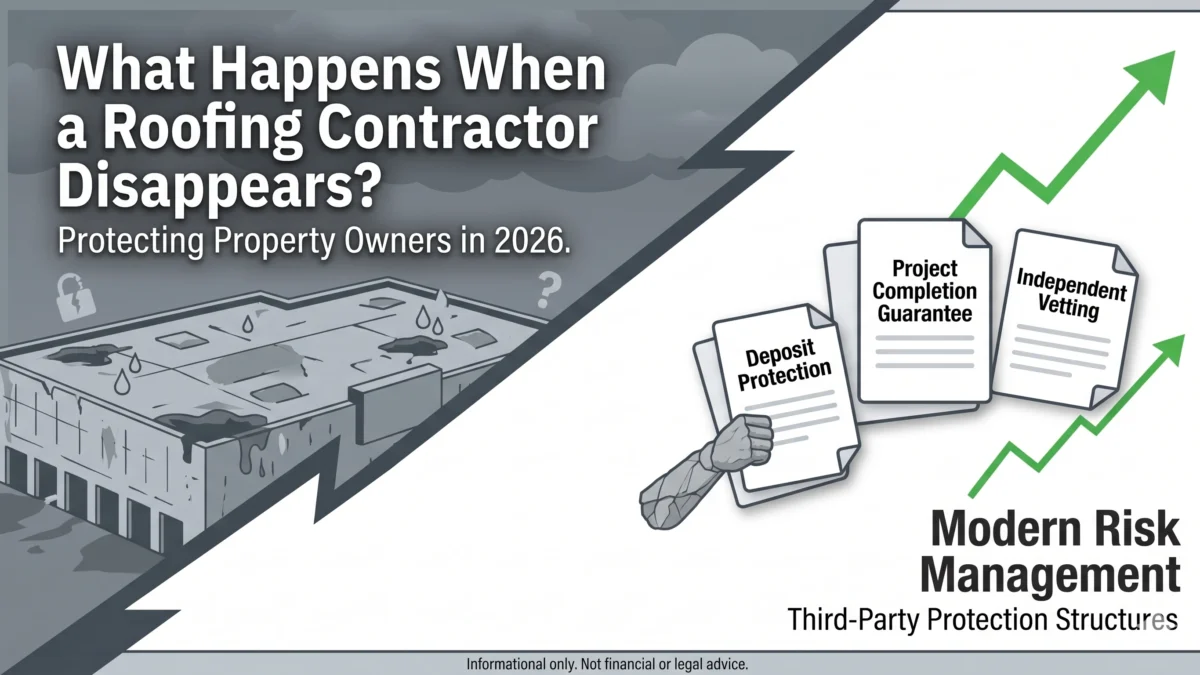

Third-Party Protection Mechanisms

In response to these risks, some projects now incorporate third-party protection programs designed to separate financial safety from contractor survival.

Depending on structure and eligibility, these programs may include:

- deposit protection (typically up to ~$30,000 depending on terms)

- project completion guarantees (in some cases $250,000+)

- contractor vetting before enrollment

The key difference is simple:

coverage is not solely dependent on the contractor staying in business.

Instead, an external entity assumes responsibility under predefined conditions.

How This Changes Risk Management for Property Owners

When properly structured, third-party protection can materially shift the risk profile of a roofing project by:

- protecting upfront investment

- reducing exposure to contractor default

- ensuring project completion under qualifying failure scenarios

- adding accountability beyond licensing and insurance alone

For commercial property owners especially, where downtime translates directly into financial loss, this layer of protection can be as important as the roofing system itself.

Why This Topic Is Becoming More Relevant in 2026

Several macro trends are increasing contractor-related risk exposure:

- rising material and labor volatility

- higher contractor turnover in competitive markets

- increased reliance on subcontracted labor models

- larger average project sizes in both commercial and high-end residential sectors

As project complexity increases, so does the importance of financial and operational risk planning.

Questions Every Property Owner Should Ask Before Signing a Contract

Before starting a roofing project, it is increasingly important to clarify:

- What happens if the contractor stops operating mid-project?

- Are deposits protected in any way beyond the contract?

- Is the warranty backed solely by the contractor or externally supported?

- What mechanisms exist to ensure project completion if failure occurs?

These questions are becoming part of modern due diligence—not exceptions.

The Shift Toward Risk-Aware Roofing Decisions

The roofing industry is gradually moving away from decisions based purely on price and material selection.

A more modern evaluation framework now includes:

- contractor financial stability

- enforceability of warranties

- presence of third-party protections

- long-term accountability structures

In this model, the cheapest bid is no longer automatically the lowest risk option.

Conclusion

Most roofing projects are completed successfully. However, when failures occur, the financial impact can be significant and difficult to recover.

This is why modern risk mitigation strategies—including third-party protection structures—are becoming more relevant, particularly in commercial and high-value residential roofing.

Ultimately, the decision-making framework is evolving.

It is no longer only about the cost of the roof.

It is also about how that investment is protected if something goes wrong.

Disclaimer

This article is for informational purposes only and does not constitute legal or financial advice. Property owners should review all contractual terms, warranty structures, and protection programs with qualified professionals before making decisions.

Here are the basic project details:

- Project Name/Location: Commercial Roof Restoration at Villa Hermosa Vista HOA in Signal Hill, CA.

- The Challenge & Solution: Other contractors insisted that a complete tear-off and roof replacement were necessary. Instead, we proposed a full restoration, saving the client $45,000.

- Scope of Work: We pressure-washed the entire 13,000 sq. ft. roof, repaired and reinforced all vulnerable areas, and applied a high-grade silicone coating. As you can see from the photos, the transformation is significant.

- Warranty & Certification: As certified installers, we were able to provide a 15-year No Dollar Limit (NDL) manufacturer warranty, backed by our own 12-year workmanship warranty and $250.000 full coverage third party guarantee via Directorii

Author Bio

Andy Markavets is a roofing contractor and co-founder of Golem Roofing, a California-based roofing company specializing in roof restoration and replacement systems. The company focuses on long-term performance solutions and risk-aware project execution for residential and commercial properties.

Website: https://golemroofing.com